UK and European economies are at an Inflection Point, finds Nicholas Brooks, Head of Economics and Investment Research, ICG, in his latest Macro Views report.

Key trends

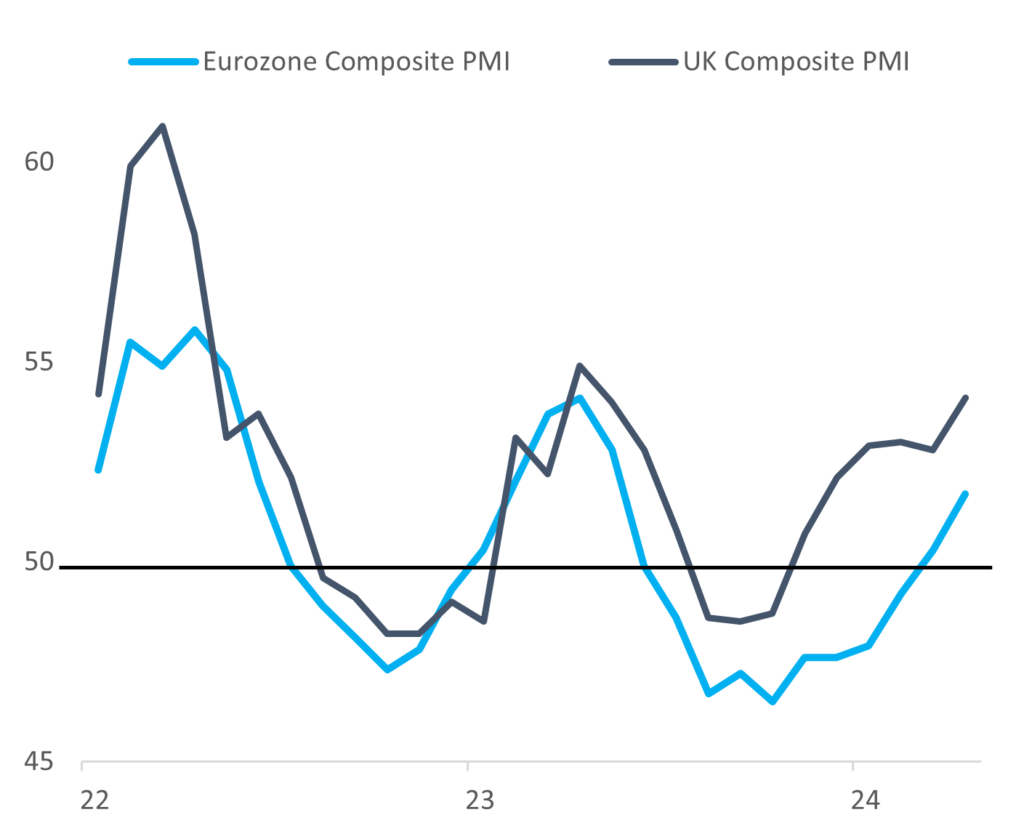

- Europe and UK economies starting to pick up. Recent macro data indicates that after over a year of lacklustre economic growth, growth momentum in continental Europe and the UK is starting to pick-up. GDP growth in Q1 rose across all major economies and purchasing manager indexes, and other high frequency data indicate the growth rebound has continued into Q2. Rising real incomes on healthy wage growth and falling prices are supporting private consumption, while a rebound in the global industrial cycle and a normalisation of energy prices and supply chains should support investment and export growth going forward. Falling interest rates should provide further growth support later this year and into 2025.

- Resilient US economy delays Fed rate cuts. The main theme of the past few quarters has been consistent outperformance of the US economy relative to Fed and consensus expectations. Some of the main drivers of this outperformance include far more expansionary fiscal policy than expected, a substantial easing of financial conditions despite Fed rate hikes, and consumers running down savings at a more aggressive pace than expected. All these factors are likely to moderate in the coming quarters, allowing the US economy to slow to a more sustainable pace and the Fed to start cutting rates later this year.

- Diverging inflation trends lead to diverging monetary policy trends. Although resilient US growth has been positive for companies’ top-lines, a negative side effect of the sustained period of above potential growth has been slower than desired progress on inflation – with services inflation proving particularly sticky due to (partial) pass-through of high wage growth. While lead indicators point to an easing of US labour market tightness, slow progress likely means Fed rate cuts are delayed until the autumn. Europe by contrast, following a period of below potential demand growth, has seen core inflation pressure ease more quickly, with ECB rate cuts likely to start in June and the BoE likely followingly shortly behind.

- Global event risk remains high. Although economies and markets have so far remained resilient, there are multiple risks that could change the current relatively benign investment landscape ranging from potential spillovers into energy markets from the Israel-Hamas war, Putin’s continued war in Ukraine, a watershed US election in November and potential for an escalatory trade war with China among many others.

- Implications for investors. In this environment of positive but sluggish growth and lower but still high interest rates, company performance dispersion is likely to continue to widen, with pricing power, cost control, balance sheet management and access to capital likely to remain key performance differentiators. In our view this should continue to favour investors with medium to long-term investment horizons, strong bottom-up analytical capabilities, the ability to provide flexible capital and work closely with portfolio companies to provide support through a continued volatile macro and geopolitical environment.

Europe and UK growth momentum picking up

Subscribe to our newsletters

Sign up for Regulatory News updates: click hereAuthors