Good morning,

Thank you to everyone who joined us at our AGM last Thursday. We appreciated the thoughtful discussion and hope those who attended found the session useful.

I (Colm) have recently returned from San Francisco, where I spent time with managers we have partnered with for a number of years, such as Hellman & Friedman, as well as newer relationships, such as Genstar and Valeas. I came away with reinforced conviction that the current pace of technological change is creating meaningful opportunities across our Portfolio and investment programme.

Implementing such technology is also a reminder of why active, long-term ownership matters. Private equity managers can work closely with management teams to prioritise investment, improve margins and adopt new tools in a disciplined way. We are seeing this within our own Portfolio.

We heard similar messages at SuperReturn in Berlin, one of the industry’s main annual gatherings. The tone was constructive but not complacent, with liquidity in particular high up the agenda for both investors and managers.

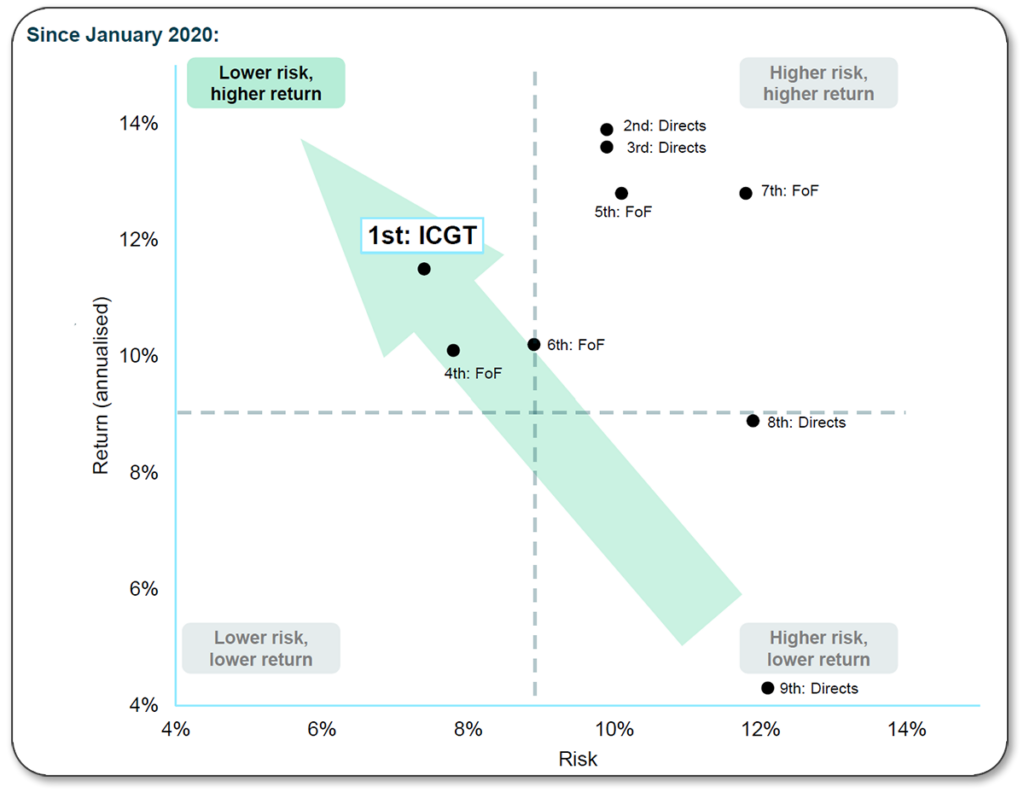

That is directly relevant to how we manage ICGT’s capital. When assessing a manager, we look carefully at how they create value, how they approach realisations and how they manage risk. Meeting managers face to face, whether in their offices or at industry events, remains an important part of that process. Our aim is to build a portfolio that compounds over the long term by investing in companies with resilient growth characteristics. Put another way, we are seeking to generate attractive returns with relatively lower volatility (or risk) than our peers. In our Q1 results presentation (available here), we shared data showing that ICGT has generated the highest NAV per Share Total Return per unit of risk among its UK-listed private equity investment trust peer group since 1 January 20201:

We believe this supports the idea that our Portfolio is delivering what we intend it to, and that ICGT can have a role in portfolios looking to generate long-term compounding growth. For those who are interested in hearing more about our investment approach, I (Colm) recently appeared on AJ Bell’s Money & Markets podcast. You can listen here.

With best wishes,

Oliver and Colm

Past performance is not a reliable indicator of future results.

Unsure of some of these terms? See our Glossary.

1 FoF = fund of funds peer. Source: Deutsche Numis, Morningstar, data accessed on 13 June 2026. 1 ‘NAV return per unit of risk’ is calculated as annualised NAV per Share Total Return divided by annualised standard deviation of those returns. Shown for illustrative peer comparison only; this is not a standard industry measure. Since January 2020, ICGT is 1st for this ratio (11.5% return / 7.4% volatility = 1.56x). The equivalent ratios of the peers range from 1.40x to 0.35x. The peer group includes HVPE, PIN, PPET, CTPE, HgT, OCI, NBPE, PEY

Subscribe to our newsletters

Sign up for Regulatory News updates: click hereAuthors